- Home

- Q&A

-

Are founders putting themselves at risk if they reveal their fundraising plans on a public forum like Twitter?

Yes! It is amazing how common it is for founders to publicly pitch investments in their companies. This is not always illegal. There are some securities exemptions under which this is allowed (e.g. Regulation Crowdfunding (but with some limitations) and Rule 506(c)). But most... more

Yes! It is amazing how common it is for founders to publicly pitch investments in their companies. This is not always illegal. There are some securities exemptions under which this is allowed (e.g. Regulation Crowdfunding (but with some limitations) and Rule 506(c)). But most founders have not consciously chosen a securities exemption so they may inadvertently be breaking the law.

less -

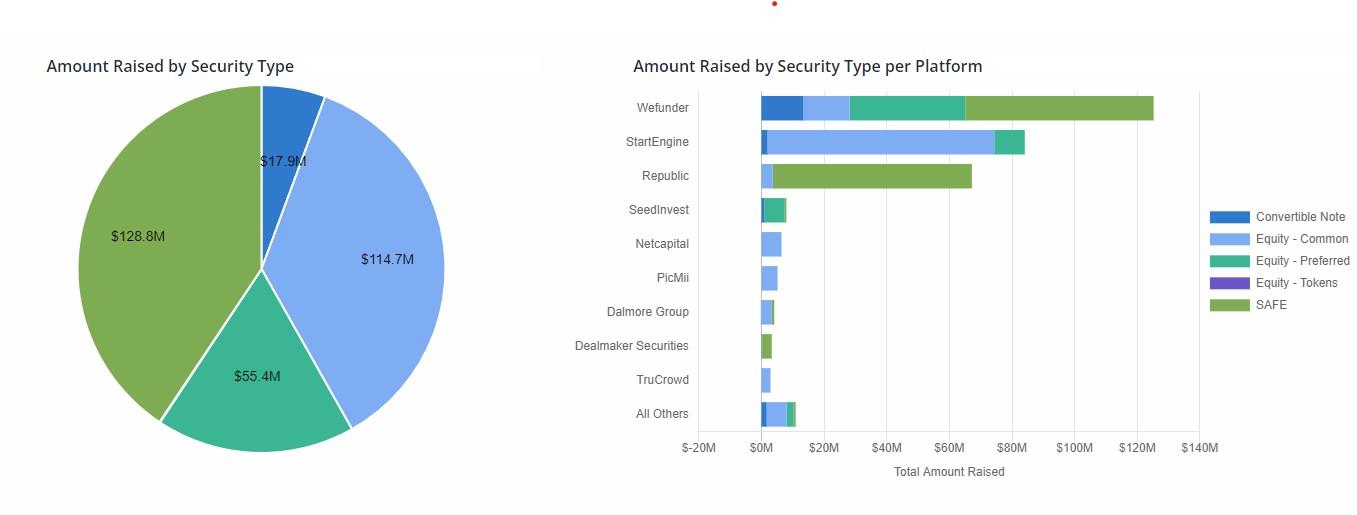

What are the type of securities used on the top Reg CF platforms?

Here is a breakdown from KingsCrowd for the most popular security types for Regulation Crowdfunding (Reg CF) in 2022 so far:

As the figures show, the most popular security types in Reg CF in 2022 are:

1. SAFE (Simple Agreement for Future Equity) - $128.8M, 41%

2. Equity (Common) - $114.7M, 36%

3. E... more

Here is a breakdown from KingsCrowd for the most popular security types for Regulation Crowdfunding (Reg CF) in 2022 so far:

As the figures show, the most popular security types in Reg CF in 2022 are:

1. SAFE (Simple Agreement for Future Equity) - $128.8M, 41%

2. Equity (Common) - $114.7M, 36%

3. Equity (Preferred) - $55.4M, 17%

4. Convertible Note - $17.9M, 6%

One can see that the type of security offered also various by platform, as platforms tend to prefer (or avoid) certain financial instruments.

For example, SAFEs are the most popular on Republic and Wefunder, while StartEngine is primarily Equity (Common).

For more details on security types in equity crowdfunding deals and their differences, check out the article I wrote here:

https://crowdwise.org/crowd-investing-101/part-4-deal-types-equity-crowdfunding/

less -

Are there any helpful crowdfunding events coming soon?

Glad to learn of your interest in regulated investment crowdfunding (#RIC).

Yes, there are a few upcoming events in the space ...

SuperCrowd22 will include a Who's Who in regulated crowdfunding and will examine the intersection of crowdfunding and impact investing. It is a web-based event bein... more

Glad to learn of your interest in regulated investment crowdfunding (#RIC).

Yes, there are a few upcoming events in the space ...

SuperCrowd22 will include a Who's Who in regulated crowdfunding and will examine the intersection of crowdfunding and impact investing. It is a web-based event being co-hosted by the Crowdfunding Professional Association (CfPA), Brainsy, and many other impactful organizations September 15-16 (registration link is here: https://www.supercrowd22.com/httpssupercrowd22comtextandpercent20otherpercent20experts-register-joinpercent20thepercent20supercrowd ) For more info, follow up with Devin Thorpe

Equity Crowdfunding Week is another event that takes place a week later in person in LA (September 21-23) or online - https://www.startupstarter.co/ecw For more info, follow up with Etan Butler

Silicon Prairie Crowdfunding often hosts webinars on Wednesdays on various topics related to crowdfunding (for beginners to experienced hands) and you can see a list of their events at: https://www.meetup.com/silicon-prairie-fundraising For more info, follow up with David Duccini

Stay tuned on the CfPA ECO as CfPA often hosts events or promotes the events of members organizations.

less -

Form C-TR question on timing of filing.

Answering a question with a question: how would engaging a transfer agent reduce the number of holders of record?

-

Do you think DAOs could replace the funding portals and investment crowdfunding?

Yes to funding portals (and probably should) and no to replacing investment crowdfunding. Rather, DAOs will most likely use investment crowdfunding to fund its projects.

-

How would you define impact crowdfunding?

Great question!

Impact crowdfunding is what is happening at the intersection of investment crowdfunding and impact investing.

As you know, investment crowdfunding was authorized by the bipartisan 2012 JOBS Act. It was initially implemented in 2016 with a $1 million cap, which was increased to $5 mil... more

Great question!

Impact crowdfunding is what is happening at the intersection of investment crowdfunding and impact investing.

As you know, investment crowdfunding was authorized by the bipartisan 2012 JOBS Act. It was initially implemented in 2016 with a $1 million cap, which was increased to $5 million last year. The space is mushrooming quickly.

Impact investing is less well known to our community but is a bigger global phenomenon dominated by wealthy families and institutions. They invest money for a financial return and a social mission. For instance, a venture capitalist backing Tesla in the early days would describe herself as an impact investor. She got a huge financial return and radically accelerated a transition to electric vehicles.

Investment crowdfunding allows for impact investing in the crowdfunding space. I call that impact crowdfunding.

SuperCrowd22 is a conference we're holding on September 15-16, 2022, to help everyone learn more about the space, both from an investor standpoint and from a social entrepreneur standpoint.

Don't miss it!

http://SuperCrowd22.com

less -

How much does it cost for a company to run a Reg CF or Reg A+ campaign?

This is a great question!

You should expect to spend about 10 percent of the money you raise on the costs of the offering, excluding marketing. I'd caution against spending money on marketing but remember it will take a lot of work.

Some legal and accounting costs will have to be paid before you can... more

This is a great question!

You should expect to spend about 10 percent of the money you raise on the costs of the offering, excluding marketing. I'd caution against spending money on marketing but remember it will take a lot of work.

Some legal and accounting costs will have to be paid before you can begin raising money. That would typically be at least $5,000 and could easily total 3 to 5 percent of the offering, depending on your circumstances.

The portal will also charge fees. They vary in structure and size but expect to pay 5 percent or more.

less -

Could blockchain be useful for the real estate industry?

Yes! Absolutely!

Many people believe, I say correctly, that one day soon, we'll use blockchain to record title to all manner of physical or tangible objects, from boats and cars to real estate. The immutable, public nature of blockchain would be perfect for this purpose.

The trick will be for the bl... more

Yes! Absolutely!

Many people believe, I say correctly, that one day soon, we'll use blockchain to record title to all manner of physical or tangible objects, from boats and cars to real estate. The immutable, public nature of blockchain would be perfect for this purpose.

The trick will be for the blockchain community to fully embrace the regulatory and governmental aspects of legal ownership of non-digital assets.

less0 -

What inspired your interest in crowdfunding?

I love crowdfunding because it helps people who traditionally have had trouble accessing capital. Women and BIPOC founders now have a new path to funding. Small businesses that are integral parts of a community, like restaurants, can now raise money from their customers. Our country is richer becaus... more

I love crowdfunding because it helps people who traditionally have had trouble accessing capital. Women and BIPOC founders now have a new path to funding. Small businesses that are integral parts of a community, like restaurants, can now raise money from their customers. Our country is richer because of crowdfunding and getting richer every day.

less- Unclassified

1 -

Good day, As a group of crowdfunding expertsI am hopeful you can steer me in the right direction. We are looking to crowdfund an Arizona permitted approved gold mining opportunity for $1,000,000, which is our immediate concern, and the next tranche would be for about...

Jordan, this is a great question. Thanks for coming to the CfPA Ecosystem for insights.

Of course, there is no industry or sector that can be thought of as traditionally raising money via crowdfunding. The industry is too new, implemented just six years ago and really gaining scale only in the past ... more

Jordan, this is a great question. Thanks for coming to the CfPA Ecosystem for insights.

Of course, there is no industry or sector that can be thought of as traditionally raising money via crowdfunding. The industry is too new, implemented just six years ago and really gaining scale only in the past two years. We're all learning.

There is no reason you can't crowdfund for a gold mining operation. Obviously, this is a great time to be investing in gold.

FINRA-registered portals are required to do some screening to prevent fraudsters from attempting to raise money on their platforms. Portals are allowed to do some additional screening to curate a theme. They are not allowed to imply that they have done thorough underwriting of an offering. Broker-Dealers, like Start Engine, that operate portals are allowed to do more and charge more than the other portals, including offering more help raising money.

Some platforms focus on serving small business, real estate, tech or other niches. While I haven't spotted a portal focused on extractive industries, one may exist. However, you can test out the large players (Wefunder, Republic and StartEngine) where you are most likely to find admission.

You want to remember that there is no magic crowd; the money you raise will come from your networks primarily.

Good luck!

less2