Tags

attorney

Latest Knowledge Board posts

Biography

Jenny has 25 years of experience as an attorney and advisor for mission-driven enterprises. She has helped her clients raise millions of dollars from values-aligned investors and raised over $1.5 million for her own businesses.

She is the author of Raise Capital on Your Own Terms: How to Fund Your Business without Selling Your Soul (Berrett-Koehler, October 2017).

Jenny earned her J.D. from Yale Law School and a masters degree in City and Regional Planning from the University of California at Berkeley.

She served on the Securities and Exchange Commission Advisory Committee on Small and Emerging Companies. She submitted the petition to the SEC that led to the passage of the 2012 JOBS Act and was present at the White House signing ceremony.

Jenny is also a fellow at Democracy Collaborative and the co-founder of the Force for Good Fund.

Before becoming a securities lawyer, Jenny worked for eleven years at a nonprofit community development corporation in Oakland, where she served as staff attorney and managed community economic development projects including the formation and management of several social ventures designed to employ and create business ownership opportunities for low-income community residents.

Jenny is the President of Community Ventures, a nonprofit organization dedicated to promoting the economic and social development of communities. She also co-founded the Sustainable Economies Law Center, a nonprofit that provides legal information to support sustainable economies.

Jenny is on the board of directors for CfPA (Crowdfunding Professional Association) and formerly served as a director of Berrett-Koehler Publishers. Jenny is certified as a coach by the International Association of Women in Coaching.

What do you think of Chat GPT's response to my query?

Could you please help me evaluate a legal question? The SEC regulates the way that private companies who are raising capital conduct their offerings. This includes those raising under Regulation Crowdfunding. I believe that there are some rules about conducting a "demo day" or live pitch event where issuers share their stories in front of investors, live or virtually. One rule I've heard is that a nonprofit should host the event. Colleges and nonprofit accelerators are obvious candidates. Can for-profit media companies host live-pitch-style events legally? If so, what are the rules?

The Securities and Exchange Commission (SEC) does indeed regulate the conduct of private companies when they are raising capital, including offerings under Regulation Crowdfunding. The rules around conducting "demo days" or live pitch events where issuers present to potential investors have specific guidelines designed to prevent these events from being considered "general solicitation," which is restricted under certain circumstances.

The specific rule that governs these events is part of Regulation Crowdfunding and the broader regulations concerning private securities offerings:

1. Role of the Host: Traditionally, demo days or similar events are hosted by colleges, universities, non-profit organizations, or incubators/accelerators without a financial interest in the offerings being presented. This setup helps ensure that the event's primary purpose isn't to advertise or sell securities, which could be construed as general solicitation.

2. For-profit Entities Hosting: For-profit entities, including media companies, can host such pitch events. However, the SEC released amendments in March 2021, clarifying and expanding the scope of permissible activities at such events. According to the amendment, issuers can speak at events sponsored by "a college, university, or other institution of higher education, a state or local government or instrumentality of a state or local government, a nonprofit organization, or an angel investor group, incubator, or accelerator." Importantly, the amendment also includes provisions for "a potential host that is neither issuing nor selling securities in connection with the event," which could include for-profit entities under certain conditions.

3. Conditions for For-profit Hosts:

- No Financial Interest: For-profit hosts should not have a financial interest in the issuers presenting at the event. This means they should not receive compensation based on investment commitments or the outcomes of the securities offerings presented.

- Event Restrictions: The events should be related to the host’s stated mission or purpose if it's an organization, and the host cannot make investment recommendations or provide investment advice.

- Communications Restrictions: Issuers can generally discuss the terms of the offering and include a factual business description of their company, but they must avoid "conditioning the market." This includes not engaging in hype or overly promotional language about the securities being offered.

4. Disclosure Requirements: If for-profit media companies host such events, they should ensure that issuers follow the disclosure requirements under Regulation Crowdfunding, including providing information about the offering on a platform that meets the requirements for such offerings.

To ensure compliance, it's advisable for for-profit media companies to consult with legal experts who specialize in securities law and the specific regulations of Regulation Crowdfunding. This will help avoid any potential violations that could arise from hosting such an event.

There is a federal exemption for Demo Days but it is useless because it doesn't preempt state law. To legally do a demo day where the public is invited, even if the event fits under the Demo Day exemption, it will still be illegal to do public solicitation under state law (unless the offering is being done under Reg CF or Rule 506(c) in which case there is federal preemption).

As far as I know Wefunder does do this, but this would be a great question to ask Wefunder. I know many offerings on Wefunder that have been channeled through a series LLC without the issuer's or the investors' knowledge. Also, every crowdfunding lawyer I have spoken to believes that Wefunder's use of the series LLC is not legal so issuers and investors need to be very careful.

The limitation on how much a nonaccredited investor can invest during a 12-month period depends on his or her net worth and annual income:

• The greater of $2,500, or 5 percent of the greater of the investor’s annual income or net worth, if either the investor’s annual income or net worth is less than $124,000; or

• Ten percent of the greater of the investor’s annual income or net worth, not to exceed an amount sold of $124,000, if both the investor’s annual income and net worth are equal to or more than $124,000.

There are no current plans to change these rules, although the dollar amounts may increase from time to time. Under Securities Act Section 4A(h), the Commission is required to adjust the dollar amounts in Section 4(a)(6) “not less frequently than once every five years, by notice published in the Federal Register, to reflect any change in the Consumer Price Index for All Urban Consumers published by the Bureau of Labor Statistics.”

Unless the portal is a licensed broker-dealer, it may not offer investment advice or recommendations or solicit purchases, sales, or offers to buy the securities offered or displayed on its platform.

It may however apply objective criteria to highlight offerings on its platform where:

(i) The criteria are reasonably designed to highlight a broad selection of issuers offering securities through the funding portal’s platform, are applied consistently to all issuers and offerings and are clearly displayed on the funding portal’s platform;

(ii) The criteria may include, among other things, the type of securities being offered (for example, common stock, preferred stock or debt securities); the geographic location of the issuer; the industry or business segment of the issuer; the number or amount of investment commitments made, progress in meeting the issuer’s target offering amount or, if applicable, the maximum offering amount; and the minimum or maximum investment amount; provided that the funding portal may not highlight an issuer or offering based on the advisability of investing in the issuer or its offering; and

(iii) The funding portal does not receive special or additional compensations for highlighting one or more issuers or offerings on its platform.

Unless the portal is a licensed broker-dealer, it may not offer investment advice or recommendations or solicit purchases, sales, or offers to buy the securities offered or displayed on its platform.

It may however apply objective criteria to highlight offerings on its platform where:

(i) The criteria are reasonably designed to highlight a broad selection of issuers offering securities through the funding portal’s platform, are applied consistently to all issuers and offerings and are clearly displayed on the funding portal’s platform;

(ii) The criteria may include, among other things, the type of securities being offered (for example, common stock, preferred stock or debt securities); the geographic location of the issuer; the industry or business segment of the issuer; the number or amount of investment commitments made, progress in meeting the issuer’s target offering amount or, if applicable, the maximum offering amount; and the minimum or maximum investment amount; provided that the funding portal may not highlight an issuer or offering based on the advisability of investing in the issuer or its offering; and

(iii) The funding portal does not receive special or additional compensations for highlighting one or more issuers or offerings on its platform.

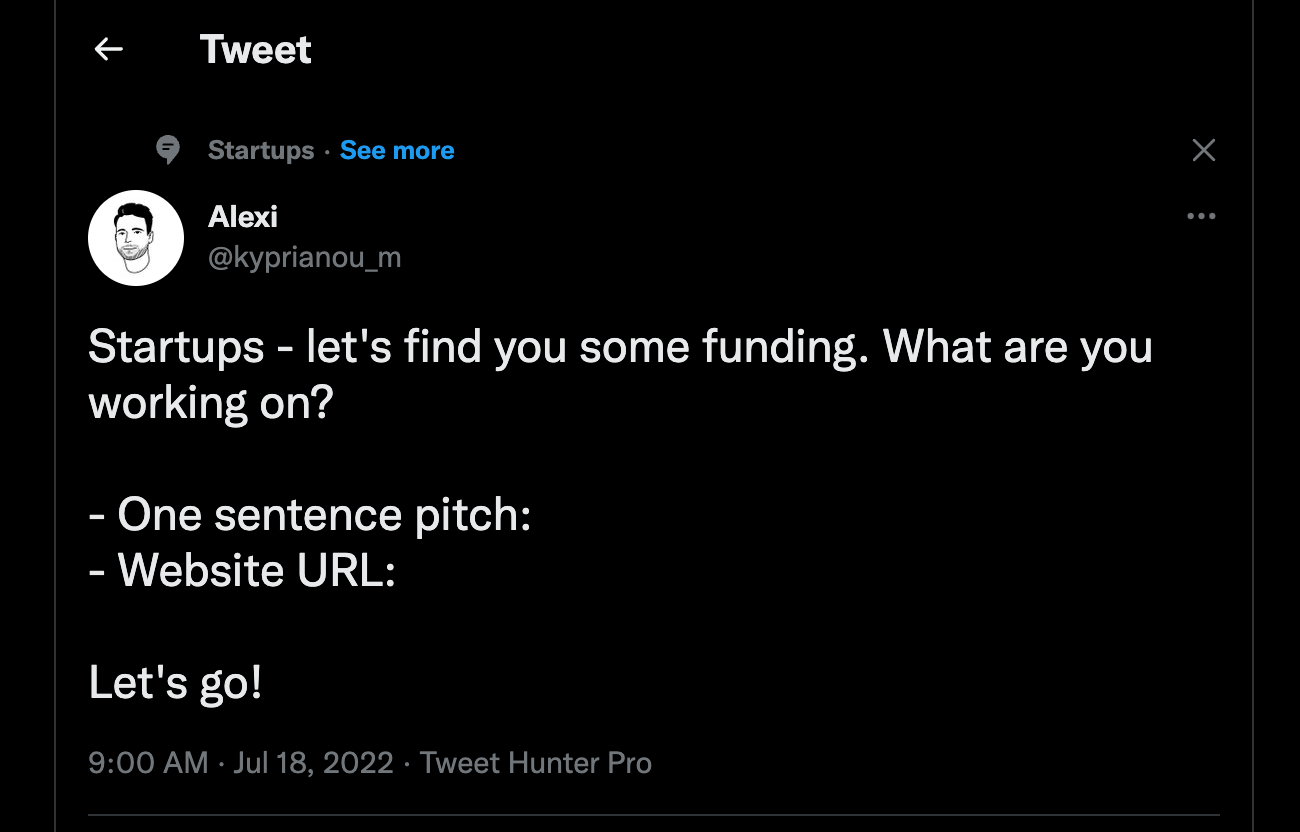

Are founders putting themselves at risk if they reveal their fundraising plans on a public forum like Twitter?

This tweet -- and the many public responses where founders publicly revealed their fundraising status and plans -- prompted the question. #crowdfundingeducation

https://twitter.com/kyprianou_m/status/1549016138515972097?s=20&t=nTu6epYBcI-euGv2X59dsQ

Yes! It is amazing how common it is for founders to publicly pitch investments in their companies. This is not always illegal. There are some securities exemptions under which this is allowed (e.g. Regulation Crowdfunding (but with some limitations) and Rule 506(c)). But most founders have not consciously chosen a securities exemption so they may inadvertently be breaking the law.

The issuer must post on its website an annual report along with its financial statements certified by the principal executive officer of the issuer to be true and complete in all material respects and a description of the financial condition of the issuer.

If, however, an issuer has available financial statements that have either been reviewed or audited by a public accountant that is independent of the issuer, those financial statements must be provided and the certification by the principal executive officer will not be required.

The annual report also must include the disclosure required by paragraphs (a), (b), (c), (d), (e), (f), (m), (p), (q), (r), and (w) of Section 201 of the Reg CF Rules.

The report must be filed no later than 120 days after the end of the fiscal year covered by the report.

The issuer must continue to comply with the ongoing reporting requirements until one of the following occurs: (1) The issuer becomes a public reporting company; (2) The issuer has filed, since its most recent sale of securities under the crowdfunding exemption, at least one annual report and has fewer than 300 holders of record; (3) The issuer has filed, since its most recent sale of securities under the crowdfunding exemption, the required annual reports for at least the three most recent years and has total assets that do not exceed $10,000,000; (4) The issuer or another party repurchases all of the securities issued under the crowdfunding exemption, including any payment in full of debt securities or any complete redemption of redeemable securities; or (5) The issuer liquidates or dissolves its business in accordance with state law.

The issuer must file with the Commission and provide to investors and the relevant intermediary a Form C: Progress Update (Form C-U) to disclose its progress in meeting the target offering amount no later than five business days after each of the dates when the issuer reaches 50 percent and 100 percent of the target offering amount. This requirement shall not apply to an issuer if the relevant intermediary makes publicly available on the intermediary’s platform frequent updates regarding the progress of the issuer in meeting the target offering amount.

The issuer must file an annual report on Form C: Annual Report (Form C-AR) no later than 120 days after the end of the fiscal year covered by the report.

An issuer eligible to terminate its obligation to file annual reports must file with the Commission, within five business days from the date on which the issuer becomes eligible to terminate its reporting obligation, Form C: Termination of Reporting (Form C-TR).

Hello! The Form C is the disclosure information that needs to be filed with the Securities and Exchange Commission before you can launch a campaign under Regulation Crowdfunding. Lawyers generally charge $5-10,000 to prepare it.

Hello! FINRA should be able to provide you with all the info you need to get properly set up. Good luck!

The costs depend on various factors. Do you need a lawyer to draft the documents for whatever security you plan to offer? Do you need help completing the Form C and making sure you do it correctly? Do you need an accountant to prepare your financials in accordance with GAAP? Do you need help with marketing and communications? These services could cost $20-25k or more. Then of course there is whatever fee the platform charges.

No! Not at all. At least they didn't INCREASE the income and wealth requirements.

Powered by Brainsy, Inc. (Patented and Patents Pending)